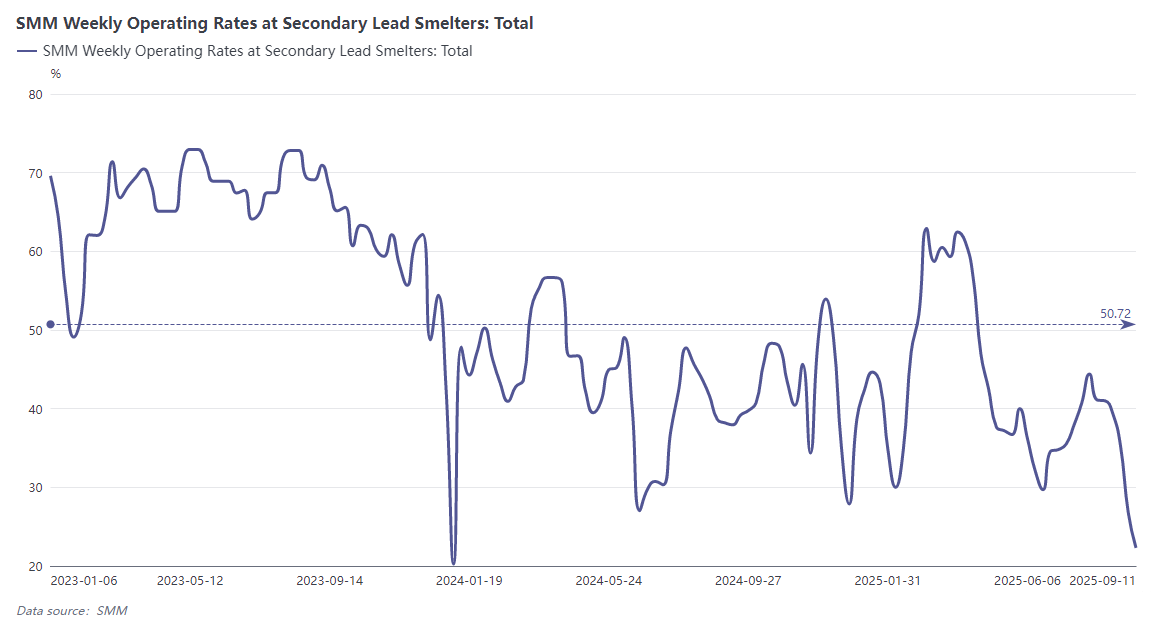

After February 2025, secondary lead smelting entered a prolonged period of losses, with raw material prices remaining high and weak end-use consumption of lead, leaving secondary lead smelters with little hope for profitability. According to SMM data, the weekly operating rate of secondary lead fluctuated between 30% and 50%, dropping below 30% in recent weeks to 22.3%, hitting a new low in nearly one and a half years.

In the current market environment where the production enthusiasm of secondary lead smelters remains low, the expectation for a recovery in operations has garnered significant attention. SMM will delve into the key dimensions of the main costs of secondary lead smelting and the performance of end-use consumption to thoroughly analyze the expectations for the resumption of operations at secondary lead smelters.

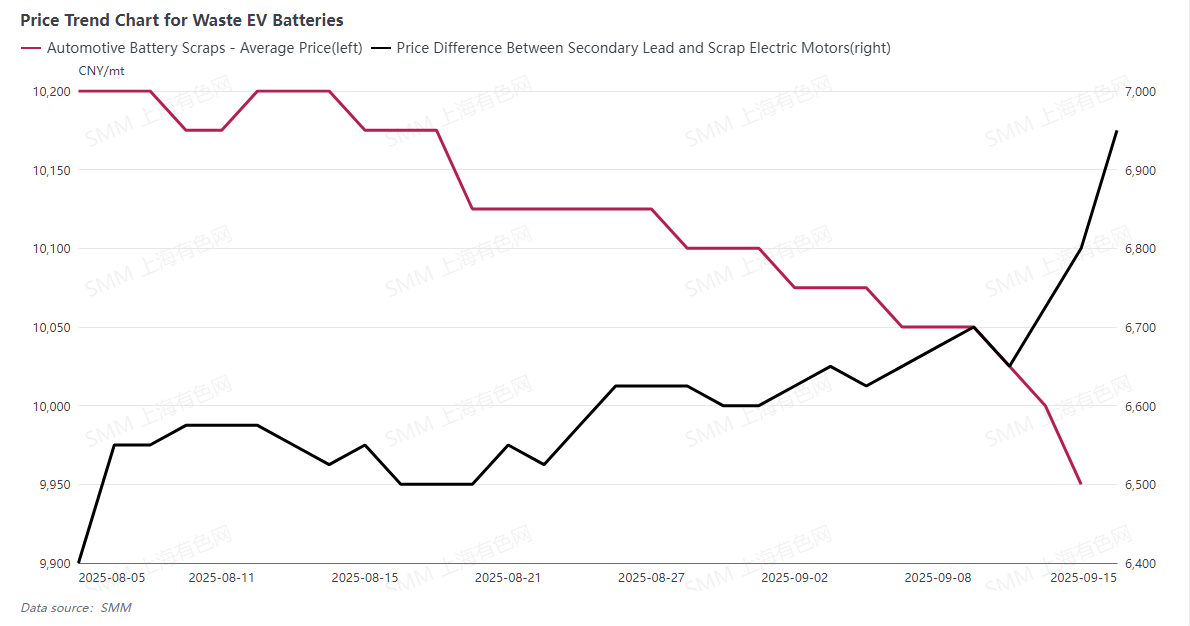

First, let's briefly review the prices of major lead-containing scrap over the past decade, using waste lead-acid EV batteries as an example.

Over the past decade, the price trend of waste lead-acid batteries used in EVs in China has been very clear, with the overall center continuously rising. Starting from 2016, as the capacity of secondary lead gradually expanded, the price of scrap batteries significantly increased. In December 2019, the outbreak of the pandemic led to a sharp decline in the industry's operating rate, with low demand for scrap batteries and prices nearing rock bottom. In January 2023, the official end of pandemic control measures was announced. As the economy gradually recovered, new secondary lead projects increased, leading to a prominent supply-demand imbalance for scrap batteries and a rise in prices. In May 2024, the implementation of the "reverse invoicing" policy for scrap batteries left recycling enterprises in a state of confusion, with most choosing to halt recycling and observe. This resulted in a sudden drop in scrap volume, and due to increased tax costs, a small number of recyclers exited the waste lead-acid battery recycling industry, pushing scrap battery prices to historic highs. After the price of scrap batteries pulled back, the center maintained an upward trend; in the past half month, there has been a slight pullback, mainly due to large-scale production cuts by secondary lead smelters, leading to a simultaneous decline in demand for waste lead-acid batteries.

The fall in scrap battery prices indicates a decrease in raw material costs for secondary lead smelters. From the chart below, the average price of scrap EV batteries has dropped by 250 yuan/mt in the past month, with a noticeable increase in the price spread between secondary lead and scrap EV batteries (a larger price spread suggests a higher likelihood of profitability for secondary lead smelters).

Additionally, the recent rebound in lead prices is also a primary driver of the widening price spread between secondary lead and scrap EV batteries.

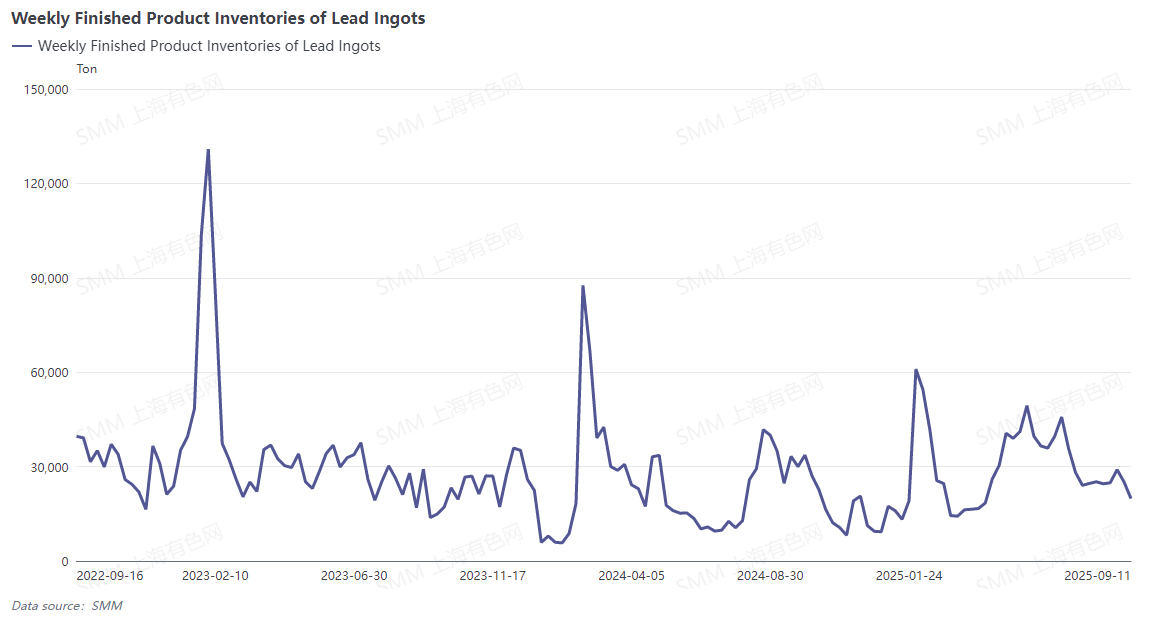

The e-bike battery market is currently in its traditional peak season, and with the implementation of new national standards for e-bikes, orders for complete vehicle sets have steadily increased. Although the battery replacement market performance varies, some enterprises can still achieve full production. The demand for lead ingots from these lead-acid battery producers has improved, and due to the high number of maintenance activities for both primary and secondary lead in September, the supply of finished products in producer's warehouses is limited, leading to firm quotes from suppliers (some suppliers, expecting future price increases, are holding back from selling).

Currently, lead ingot finished product inventories are limited, while social inventories of lead ingots have risen as expected due to the arrival of delivery supplies at warehouses. With only half a month left until the Mid-Autumn Festival and National Day holidays, downstream enterprises traditionally stockpile lead ingots as needed before the holidays. Social inventories of lead ingots may reverse their trend and pull back, and in the short term, lead prices are expected to hold up well.

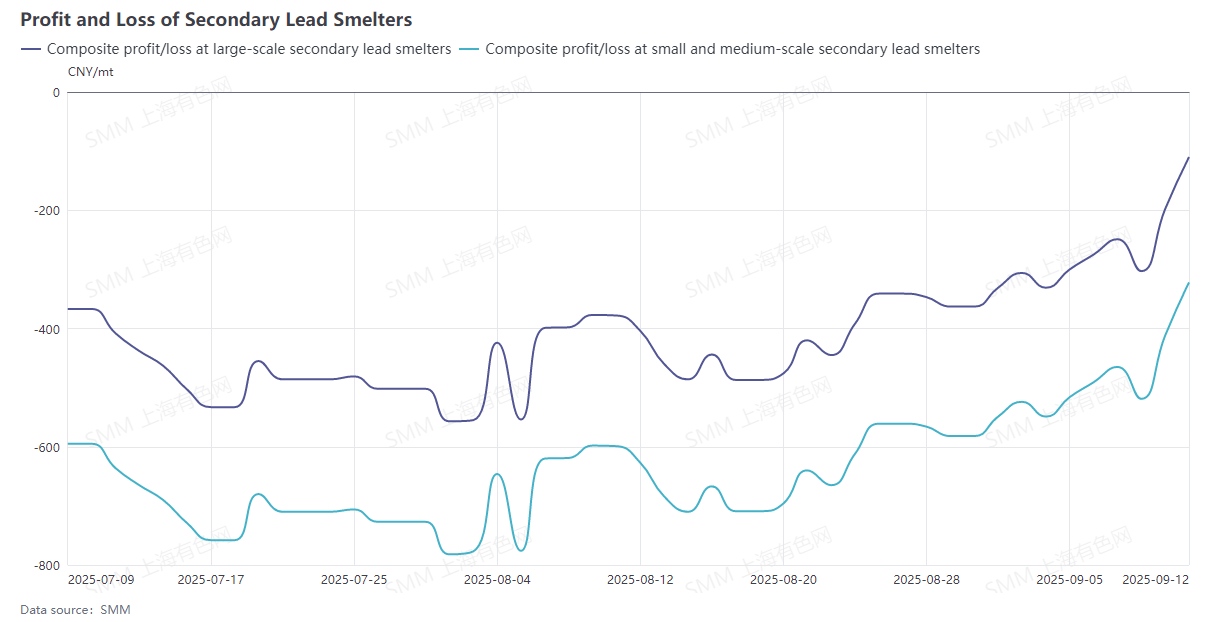

According to the latest data from SMM’s secondary lead profit model, although secondary lead smelting profits have not yet turned positive, the loss margin has significantly narrowed. This has provided some boost to the production enthusiasm of secondary lead smelters.

Although consumption of lead-acid batteries for e-bikes is currently favorable, the performance of other battery types varies. Orders for ESS battery enterprises remain relatively stable, though some export orders have shown fluctuations. The automotive battery market is performing weakly, with dealers experiencing slow inventory digestion. Coupled with the impact of tariffs on battery export orders, the operating rates of some producers have dropped to 50-60%, or even below 50%. It is necessary to monitor the actual intensity of pre-holiday stockpiling by downstream enterprises and its impact on lead price trends.

In summary, recent scrap battery prices have stabilized after a decline. With improving consumption of e-bike batteries and a rebound in lead prices, secondary lead smelting profits are nearing breakeven. Additionally, due to the upcoming Mid-Autumn Festival and National Day holidays, the customary stockpiling by downstream enterprises is expected to support lead prices. SMM believes that the willingness of secondary lead smelters to resume production may gradually increase. Currently, several idled secondary lead smelters have tentatively scheduled production resumptions for early October.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM’s internal database model, and are for reference only, not constituting decision-making advice.